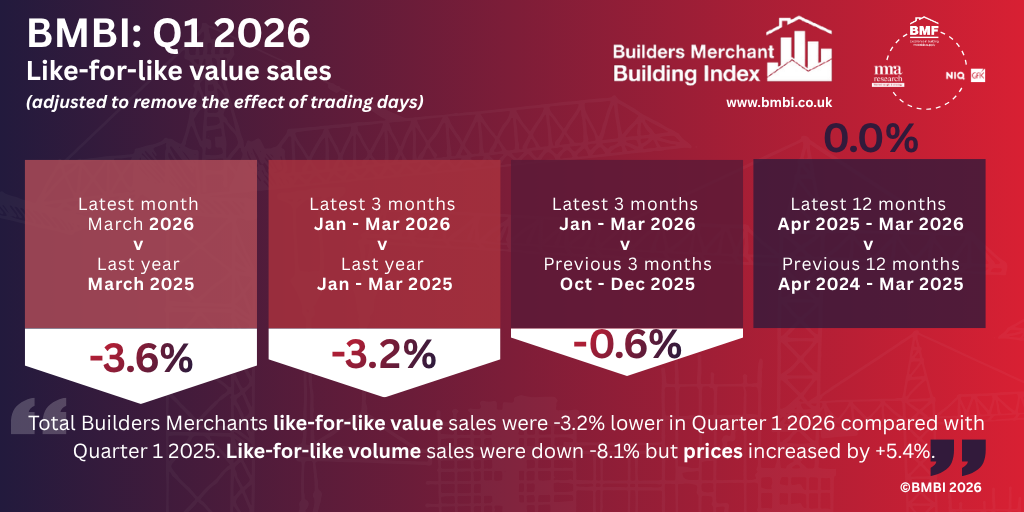

The latest Builders Merchant Building Index (BMBI) report reveals Total Builders Merchants like-for-like value sales for Q1 2026, adjusted to remove the impact of trading days, were -3.2% lower than Q1 2025. Like-for-like volume sales were down -8.1%, with prices increasing +5.4%.

Emile van der Ryst, Senior Client Insight Manager at NIQ GfK, commented: "Early optimism for 2026 has faded as the wider UK construction market continues to face significant headwinds. Growth forecasts have been revised down, construction output has weakened, particularly in private housing, and merchants have reported falling sales during the opening months of the year.

"Against this backdrop, Builders Merchants recorded a -3.2% decline in value in Q1 2026 compared to Q1 2025. Volumes fell noticeably by -8.1%, with average pricing up by +5.4%. This is a continuation of a trend starting in November where volumes declined and average pricing increased. January and February were especially affected by wet weather, resulting in double digit volume declines.

"Heavy Building Materials was a key driver behind this, down -6.7% in value. Volumes were down -11.8%, with average price up +5.7%. These volume declines were seen across almost all subcategories, but those in aggregates, blocks, bricks and roofing products stood out. Landscaping was the other key area to see a noticeable negative shift, as value from 2025 Q1 to 2026 Q1 dropped by -7.0%. Landscaping subcategory fencing and gates had the largest negative value impact across all major subcategories.

"Timber & Joinery remained an area of strength for the sector, up +0.9% in Q1. Timber and sheet materials both saw value growth, but it's worth mentioning the former was driven by average price increases, the latter by volume growth. Cladding performance stood out, with this being one of the best performing subcategories across all areas.

"In the smaller categories, double digit growth took place in Renewables and Water Management, with noticeable growth also seen in Workwear and Safetywear. Kitchens and Bathrooms increased +1.8% in value, while Plumbing, Heating and Electrical was up +0.1%. The former benefitted from growth in both bathrooms and fitted kitchens, with the latter helped by boilers, tanks and accessories.

"Looking ahead, uncertainty remains elevated, feeding into growing concerns around housebuilding targets and the need for governmental intervention."

John Newcomb, CEO of the Builders Merchants Federation, added: "Early signs of improvement in construction output in February were quickly reversed after the start of the Middle East conflict in March. The expectation now is that the conflict will further intensify pressures, particularly through rising prices and renewed inflation.

"The latest ONS figures estimate that total construction output grew by +0.4% in Q1 2026 compared with Q4 2025. However, total construction new orders fell by -10. 5% in Q1 2026 over Q4 2025. At a sector level, four of the nine sectors grew in Q1, with the main positive contributor being private housing repair and maintenance, which increased by +4.1%, albeit from a low base.

"Activity in this vital RMI area was already subdued in 2025, as uncertainty ahead of the Autumn Budget led homeowners to focus on saving rather than on discretionary spending. Political and economic uncertainty, both nationally and globally, coupled with the adverse effect of inflation on household bills, means this "wait and see" approach is expected to continue for the next 12 months.

"Private housing is also performing below expectations. Although annual home completions rose for the second consecutive quarter at the start of the year, with Energy Performance Certificate data showing that 204,500 homes were completed in the 12 months to March 2026, this is a very marginal improvement (1%) on Q4 2025.

"On top of this, housing starts have continued to fall, indicating that future housing delivery will be little better. National House Building Council (NHBC) show starts fell by -4% between January and March 2026 and are down -3% on an annual basis.

"Housing supply remains considerably below what's needed to meet either the Government's calculation of housing need in England (c. 367,000) or its target of delivering 1.5 million new homes.

"At this stage, it is difficult to envisage a significant upturn in the coming year without government action to speed up planning and provide incentives to unlock the housing market."